Ari isn’t just a trader—he’s a phenomenon. Born with an instinct for probabilities and a mind wired for strategy, Ari turned sports betting into an art form and commodities trading into a science. Expelled from business school for playing too close to the edge? He calls it a badge of honor—a reminder that rules are for people who can’t beat the game.

Senior Analyst & Trader

Brando W.

“25-Year-Old Trading Visionary”

At just 25 years old, Brando has shattered expectations in the world of options trading and predictive market strategy. Renowned for her ability to forecast volatility and price movements with surgical precision, Brando has mastered the art of transforming risk into opportunity. Her approach is fearless, data-driven, and unapologetically focused on winning.

Brando’s expertise lies in predictive trading, where she harnesses advanced analytics, behavioral modeling, and real-time market intelligence to anticipate trends before they emerge. Beyond the trading floor, Brando designs hedging frameworks for agriculture, protecting feedlots and agribusinesses from market shocks while unlocking new profit streams.

Options Desk Manager:

Seraphina Gold

“The Queen of Odds”

Seraphina Gold doesn’t play the market—she bends it to her will. At 30, she’s already a legend in the options game, turning volatility into her personal playground. While others panic over price swings, Seraphina thrives on chaos, stacking wins like chips at a poker table. Her obsession? Sports betting and options trading—because why settle for one arena when you can dominate both?

Predictive Market Consultant

Moses

“The Spread King”

Moses didn’t just grow up in the Bronx—he grew up hustling odds. At 45, he’s the guy Wall Street whispers about when cattle spreads start moving. While most traders stick to vanilla strategies, Moses thrives in the complex world of options, cattle crush spreads, and credit default swaps. He’s not here to play safe—he’s here to dominate.

Every trade is a calculated ambush. He sees risk where others see chaos and turns it into profit with surgical precision. Moses doesn’t follow the market; he writes the playbook. From hedging feedyard margins to structuring swaps that make banks sweat, his game is pure strategy and swagger. If you’re looking for boring, look elsewhere. If you want to learn how the best turn volatility into victory, Moses is your guy.

🔁 5. Double Calendar or Iron Condor (Expecting Sideways Price Action)

Double Calendar: Buy both long-dated call and put calendars around ATM—they benefit from emerging volatility ahead of events. [tradingview.com]

Iron Condor: Sell an OTM call and put, buy further OTM protective wings. Profits from price stability and declining volatility.

📊 6. Skew-Based Trades (Directional Tilt)

Analyze 25-delta skew: if calls are cheap relative to puts, consider call spreads; if puts are expensive, benefit from put spreads or credit spreads. [cboe.com], [marketchameleon.com]

📌 Suggested Tacticals for Today

Market View

Strategy

Rationale

Volatility spike expected

Long Straddle, Double Calendar

Capture moves and IV increase

Bullish outlook (rate cut + supply risk)

Bull Call Spread

Cheaper bullish exposure

Bearish outlook (inventory up, demand soft)

Bear Put Spread

Downside protection

Neutral/range-bound

Calendar Spread, Iron Condor

Profit from time decay and low volatility

🔎 Execution Tips

Choose near-term expirations (e.g., Jan/Feb) for straddles/spreads to capture short-term moves.

Monitor CVOL (≈31.6%)—moderate vol offers better premium for spreads vs pure volatility plays. [cmegroup.com]

Adjust strikes based on key technical levels—support around $58, resistance near $62+.

Use defined-risk structures (spreads) to manage high-cost uncertainty.

Oil prices gained following U.S. seizure of a sanctioned Venezuelan tanker; Brent rose by $0.27 (≈0.4%) to $62.48, and WTI climbed $0.33 (≈0.6%) to $58.79. [money.usnews.com], [cnbc.com]

Earlier surge of roughly 1.3% (~75¢) occurred when news broke, as traders priced in elevated geopolitical risk. [nbcnews.com], [cnbc.com]

⚠️ Geopolitical & Supply Implications

The action escalates geopolitical tensions with Venezuela, potentially constricting crude supply if shippers avoid sanctioned vessels—leading to a mild risk premium in prices. [bloomberg.com], [politico.com]

Analysts suggest the impact is short-term, with markets weighing U.S. intentions to keep oil prices under control. [bloomberg.com], [dailymail.co.uk]

🚢 Shipping Market Effects

Tanker charter rates are already elevated due to global shipping disruptions and sanctions, climbing around 467% year-to-date. [oilprice.com], [oilprice.com]

This seizure adds extra pressure on vessel availability and further strains freight capacity, possibly raising logistics costs that could filter through to crude pricing. [oilprice.com], [money.usnews.com]

🔍 What It Means for Markets

Expect modest upside in oil prices, with Brent and WTI likely to hold elevated levels (Brent $62–63, WTI near $59). [money.usnews.com], [cnbc.com]

Heights of gains depend on whether more seizures follow or if shipping firms escalate avoidance of Venezuelan tankers.

Logistics bottlenecks from tighter tanker markets could increase freight costs, subtly lifting crude price structures.

Overall, this event supports near-term bullishness in oil, primarily via risk premium and tighter shipping dynamics. Unless further escalation occurs, price moves will likely remain moderate, with focus on geopolitical developments and freight costs.

Let me know if you’d like intraday price tracking or alerts for oil or tanker-related news.

Rate-driven demand potential with manageable risk/reward

1.Precious Metals (Gold & Silver)

Silver surged to record highs—Indian silver futures jumped ~2% (₹1.91 lakh/kg), while COMEX silver hit ~$62/oz—on strong demand driven by rate-cut anticipation and tight global supply. [outlookbusiness.com], [investmentnews.com]

Gold also rallied on the dovish shift in Fed policy, benefiting from portfolio flows away from yield-bearing assets. [kitco.com], [monetamarkets.com]

Why trade today? Momentum is robust, technicals show breakouts, and a softer USD/fewer rate hikes support further gains. High liquidity and clear trend signal make these markets ideal for momentum or breakout strategies.

Why consider it? Lower interest rates can spur economic activity and demand for fuel. With oil near solid technical support, momentum traders could capitalize on this sentiment shift—though supply-side volatility is still a concern.

⚠️ Risk & Strategy Tips

Metals: monitor overbought conditions—consider breakout trades with stops below support.

Today, precious metals stand out as the strongest trade—driven by clear macro catalysts and momentum. Oil offers a solid secondary option, followed by livestock for those targeting ag spreads or early momentum plays.

Rate cut: The Federal Reserve’s Federal Open Market Committee (FOMC) lowered the federal funds rate by 25 basis points, moving it from 3.75–4.00% down to 3.50–3.75%—marking the third consecutive cut since September 2025. [cbsnews.com], [wsj.com]

Split vote: The decision passed by a 9–3 margin, with three dissenting votes—two regional presidents (Chicago’s Goolsbee and Kansas City’s Schmid) who preferred no cut, and Governor Stephen Miran, who pushed for a larger 50bps reduction. [thehill.com], [cnbc.com]

Forward guidance: The Fed highlighted that future rate cuts will depend on incoming economic data, indicating a cautious approach. The “dot plot” projects just one more cut in 2026. [cbsnews.com], [cnbc.com]

Balance sheet actions: Alongside the rate cut announcement, the Fed said it will resume Treasury bill purchases, starting with $40 billion on Friday, in an effort to support liquidity. [cnbc.com], [cnbc.com]

Powell’s message: Chair Jerome Powell described the decision as a “close call,” emphasizing a balancing act between supporting employment and managing inflation, and noting there’s “no risk‑free path” ahead. [cnbc.com], [usnews.com]

Reduced Financing Costs for Feedlot Loans

Lower interest expenses on operating and feeder cattle loans — Feedlot operations often rely on variable-rate debt for purchasing feeder cattle and financing feedlot inventories. With rate cuts, variable loan rates will drop, reducing interest costs per animal. — In recent high-rate environments, average feeder cattle loan interest reached ~9%. Even a moderate cut of 100 bps could produce meaningful savings on large-scale feedlot borrowing. [kansascityfed.org], [utbeef.tennessee.edu][terrainag.com], [kansascityfed.org]

🥩 Margin Relief During Tight Profitability

Eases pressure on already squeezed feedlot margins — High interest expenses have been contributing to negative margins in feedlots as cattle prices haven’t kept pace. — Reduced funding costs provide direct relief, especially if feed prices remain stable, potentially returning operations to breakeven or profitability. [kansascityfed.org], [utbeef.tennessee.edu]

💵 Input & Capital Costs: A Mixed Picture

Short-term operating costs ease, but capital costs may trend differently — Rate cuts lower costs of short-term credit for variable operations and livestock. — However, long-term loans (e.g., for land acquisition, feedlot expansion, or equipment) may remain expensive, as bond markets price in inflation and maintain higher long-term yields. — Feedlots bracing for infrastructure investment could still face high borrowing costs. [agrolatam.com], [conterraag.com]

🌍 Weaker Dollar → Boost to Exports

Potential rise in beef exports can support feedlot demand — Rate cuts often weaken the U.S. dollar, making U.S. agricultural exports more competitive on the world stage. — Stronger demand abroad could bolster domestic cattle prices and feedlot fill rates. [agweb.com]

Bottom Line for Feedlots into 2026

Short-term: Reduced interest rates offer tangible savings on working capital, improving cash flow and easing margin pressures amid tight feedlot economics. Strategic/Cautious: Long-term borrowing remains risk-laden. Feedlot operators should continue conservatively evaluating expansion or capital investment decisions. Tailwind: Potential for stronger export-driven cattle demand, further aiding feedlot market conditions.

In recent months, the New World screwworm has dominated headlines in cattle markets, painted as a looming biological threat capable of devastating herds. But let’s look deeper: is this truly about animal health, or is it a well-timed scare tactic designed to influence market behavior?

The parasite is real—but the narrative surrounding it often feels amplified at critical points in the cattle cycle. When feeder supplies are already tight, fear-driven messaging about disease risks can justify aggressive policy moves, such as halting Mexican feeder imports. That single action constrains supply, drives up domestic feeder prices, and reshapes regional feeding dynamics. For traders, this isn’t just biology—it’s economics. Every headline that screams “catastrophe” injects uncertainty into the market, and uncertainty is the fuel for volatility.

Here’s the reality: the screwworm issue has been contained before, and eradication protocols exist. Yet the timing of these alerts—coinciding with seasonal placement lows and packer margin shifts—suggests more than coincidence. It creates a psychological premium, pushing futures higher and rewarding those positioned for scarcity. In short, the screwworm story isn’t just about worms—it’s about leverage. Recognizing this dynamic is critical for predictive traders who understand that markets move on perception as much as fundamentals.

📅 What the December 19 USDA Cattle on Feed (COF) report will cover

USDA‑NASS typically publishes COF on the third Friday of each month. The December 19 report will show feedlot inventories as of December 1, plus November placements, marketings, and other disappearance for 1,000+ head lots across the 16 largest feeding states. [nass.usda.gov]

🔢 My detailed pre‑report prediction (ranges + point estimates)

Headline (U.S. total, 1,000+ head lots):

On feed, Dec 1:11.66–11.74 million head(point estimate: 11.70 million; ≈ –1% to –2% YoY). Basis: November 1 was 11.706 million; tight feeder supplies and modestly lower net inflows suggest another small drawdown into December. [esmis.nal.usda.gov]

Placements (Nov):1.74–1.82 million head(point: 1.78 million; ≈ –6% to –12% YoY). Basis: The Mexico feeder import halt has constrained fall inflows; October placements were already down 10% YoY to 2.039 million, the lowest October on record. With seasonally smaller November placements, another decline is likely. [fb.org], [esmis.nal.usda.gov]

Marketings (Nov):1.73–1.77 million head(point: 1.74 million; ≈ –1% to –4% YoY). Basis: October marketings were 1.697 million (–8% YoY), and while weekly slaughter briefly ramped early December, November’s full‑month marketings likely stayed below last year given tighter front‑end supplies. [esmis.nal.usda.gov], [cattlerepo…center.com]

Other disappearance (Nov):50–60 thousand head(point: 55k), in line with recent months. [esmis.nal.usda.gov]

Arithmetic check (point estimates): Dec 1 on‑feed ≈ 11.706 + 1.780 – 1.740 – 0.055 = 11.691 million head, rounded to ~11.69–11.70 million. [esmis.nal.usda.gov]

🧠 Why these numbers make sense (drivers & context)

1) Tight feeder supplies, especially in the Southwest

US feeder cattle imports from Mexico remain sharply constrained due to New World screwworm restrictions, materially reducing placements in border‑adjacent feeding regions and contributing to the Texas/Nebraska on‑feed shift seen in November. Expect that to persist in December. [fb.org], [extension….sstate.edu]

In the November COF, Texas fell ~9% YoY to 2.63 million, while Nebraska hit a record 2.64 million, overtaking Texas. The same structural constraints imply continued relative strength in Nebraska vs. Texas into December. [beefweb.com]

2) Recent COF trend is lower placements/marketings

The November 1 report showed on‑feed 11.706 million (–2% YoY), October placements 2.039 million (–10%), and October marketings 1.697 million (–8%)—consistent with smaller calf crops and constrained inflows. November should echo that pattern at slightly smaller absolute levels. [esmis.nal.usda.gov]

3) Packer capacity headlines don’t change the November math

Tyson’s Lexington closure (effective early 2026) and Amarillo shift reduction are a big story for forward capacity/competition, but they do not reduce November marketings captured in the December COF. Near‑term, those moves temper the price outlook and could cap futures’ response to bullish supply prints. [bloomberg.com], [amarillo.com], [cattlerange.com]

4) Slaughter cadence vs. calendar

Early December saw a weekly slaughter spike (~600k head), but the December COF reports November flows. While packers pulled harder as margins improved, the November total looks below year‑ago given the 12‑month downtrend in feedlot inventories. [cattlerepo…center.com], [farmprogress.com]

📦 Placement weight mix & heifers (what to look for)

Weights: Expect a relatively heavier skew (700–899 lb) in November placements compared with deep‑fall history, as fewer light calves are available. For reference, October’s distribution was 515k (<600 lb), 420k (600–699), 445k (700–799), 384k (800–899), 195k (900–999), 80k (1000+)—November should be the same shape at lower totals. [esmis.nal.usda.gov]

Heifers: The steer/heifer split is formally reported quarterly (next in January). Recent analysis shows fewer heifers on feed YoY largely because Mexican spayed heifers vanished from the pipeline after the border closures—not a definitive sign of aggressive domestic heifer retention. Keep that nuance in mind when interpreting January’s ratios. [southernagtoday.org], [cattlerange.com]

🧭 Likely market reaction (base case)

Futures: A modestly bullish knee‑jerk (tight supplies), tempered by the 2026 packer capacity narrative and USDA’s lowered price outlook through 2026 in WASDE. Expect choppy trade with deferreds lagging if traders view capacity cuts as demand‑side headwinds for cattle prices. [bloomberg.com]

Cash: Firm to slightly higher where negotiated trade can clear; regional spreads may widen with Nebraska/Iowa stronger than Texas/Kansas if on‑feed dispersion persists. [beefweb.com]

Boxes & kill: Short holiday weeks will mute late‑December slaughter, but early January data will start reflecting packer network adjustments. [cattlerepo…center.com]

🎯 Trader’s checklist for December 19 (Plains People style)

Pre‑position sizing: Keep risk light into the print; widen stops around the release window. Volatility clusters around COF drops.

What matters most:Placements vs. last year and Dec 1 on‑feed—anything near the low end of the ranges above is bullish.

Regional basis: Nebraska‑centric strength vs. Texas—check your packer bids accordingly. [beefweb.com]

Forward curves: If the report prints tight, look for front‑month support; but don’t ignore the capacity story capping deferreds. [bloomberg.com]

Next catalyst:January COF (quarterly steer/heifer) + Jan 31 cattle inventory—key for heifer retention signals and 2026 calf crop expectations. [nass.usda.gov]

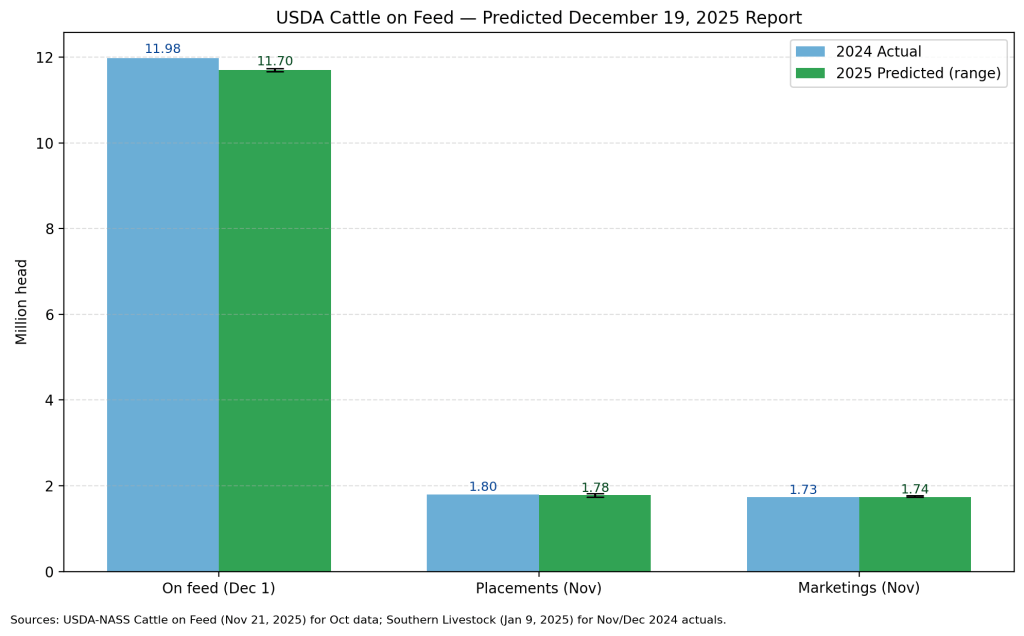

What’s shown

On feed (Dec 1, 2025) — Predicted:11.70 M head Range:11.66–11.74 M

Placements (Nov 2025) — Predicted:1.78 M head Range:1.74–1.82 M

Marketings (Nov 2025) — Predicted:1.74 M head Range:1.73–1.77 M

2024 comparison (Dec 2024/Nov 2024 actuals): On feed 11.98 M, Placements 1.80 M, Marketings 1.73 M[us-prod.as…rosoft.com]

Sources & basis

USDA-NASS COF (Nov 21, 2025) for latest verified October and November 1 figures (on-feed 11.706 M; October placements down 10%; October marketings down 8%). These anchor the trajectory into December. [cfbf.com]

Southern Livestock (Jan 9, 2025) for Nov/Dec 2024 actuals used as comparison bars (Dec 1 on-feed 11.98 M; Nov placements 1.80 M; Nov marketings 1.73 M). [us-prod.as…rosoft.com]

Constraints on Mexican feeder imports (New World screwworm restrictions) inform the tighter placements outlook. [rfdtv.com], [producer.com]

Minimum-price hedge (Buy puts) at/near-the-money (e.g., LEG6/LEJ6 ATM). Keeps spring upside if basis pops, defines floor.

Bear put spread (e.g., buy 227 put, sell 220 put) to cut premium while protecting normal downside.

Weekly puts (Monday expiries) around USDA Cattle on Feed/holiday windows to cheaply target event risk.

LRP endorsements (if margin is tight or cattle under forward agreements): newer 2026 rules allow coverage tied to purchase agreements; no margin calls, subsidized premiums.

Q4 2026 (Oct/Dec) – Seasonally softer, lean more protective

Short futures (LEV6/LEZ6) for pens within 60–90 days of sale; simplest way to lock price in a softer seasonal window. Manage basis actively.

Three‑way fence (buy put / sell lower put / sell OTM call) for low‑cost floors when you’re comfortable capping upside in holiday rallies.

Serial/weekly options to match exact ship weeks and avoid paying time value longer than needed

![[us-prod.as…rosoft.com]](https://us-prod.asyncgw.teams.microsoft.com/v1/objects/0-wus-d3-4d628b36316175d11925ecb8a964c440/views/original/dec19_cof_prediction.png){kind=link}